Featured

Table of Contents

Adapting to High-Interest Environments in Bloomington Credit Card Debt Consolidation

Credit card balances in 2026 have reached levels that need more than just minimum payments. For lots of households in Bloomington Credit Card Debt Consolidation, the increasing cost of living has actually squeezed monthly margins, causing a rise in revolving debt. Managing these balances includes more than just budgeting-- it needs a strategic shift in how interest is handled. High interest rates on credit cards can create a cycle where the principal balance hardly moves regardless of consistent payments. Professional analysis of the 2026 monetary climate recommends that rolling over debt into a structured management strategy is becoming a basic move for those seeking to regain control.

The existing year has actually seen a shift towards more official debt management structures. While consolidation loans were the primary choice in previous years, 2026 has seen an increase in making use of nonprofit debt management programs. These programs do not include securing a new loan to settle old ones. Rather, they concentrate on restructuring existing commitments. Success in debt decrease typically starts with expert know-how in No-Credit-Impact Relief. By dealing with a Department of Justice-approved 501(c)(3) not-for-profit firm, people can access settlements that are generally unavailable to the public. These companies work directly with financial institutions to lower rate of interest and waive late charges, which allows more of each payment to go toward the primary balance.

Mechanics of Debt Management Plans in 2026

A financial obligation management program functions by consolidating several monthly charge card payments into one single payment made to the therapy firm. The agency then disperses these funds to the various creditors. This system streamlines the process for the customer while ensuring that every creditor gets a payment on time. In 2026, these programs have become more advanced, frequently integrating with digital banking tools to provide real-time tracking of financial obligation reduction progress. For residents in various regions, these services supply a bridge in between frustrating debt and financial stability.

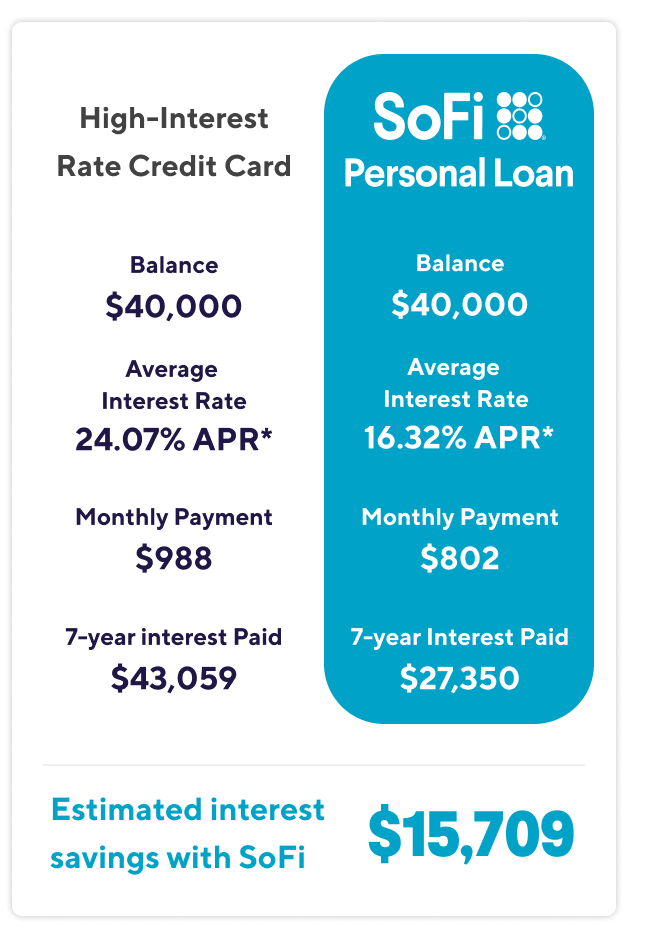

The negotiation phase is where the most substantial cost savings happen. Lenders are frequently ready to offer concessions to nonprofit agencies since it increases the likelihood of complete payment. These concessions might include dropping a 24% rates of interest to 8% or lower. This decrease significantly alters the mathematics of debt payment. Effective No-Credit-Impact Relief offers a clear roadmap for those having a hard time with multiple financial institutions. Without these worked out rates, a customer might spend years settling a balance that could be cleared in three to five years under a managed plan. This timeline is a vital factor for anybody planning for long-lasting objectives like homeownership or retirement.

Comparing Debt Consolidation Loans and Nonprofit Therapy

Picking in between a consolidation loan and a financial obligation management strategy depends upon credit health and existing earnings. In 2026, credit requirements for low-interest personal loans have tightened up. This leaves lots of people in different parts of the country searching for alternatives. A consolidation loan is a new debt that pays off old debt. If the interest rate on the new loan is not considerably lower than the average of the charge card, the advantage is minimal. In addition, if the underlying spending routines do not alter, there is a threat of adding the charge card balances again while still owing the consolidation loan.

Not-for-profit credit counseling agencies offer a various method. Because they are 501(c)(3) organizations, their main focus is education and financial obligation reduction rather than revenue. They offer free credit counseling and pre-bankruptcy counseling for those in alarming straits. Discovering reliable Debt Relief in Bloomington Minnesota can indicate the distinction between insolvency and healing. These agencies also handle pre-discharge debtor education, guaranteeing that people have the tools to avoid duplicating previous mistakes. This educational component is often what separates long-term success from temporary relief.

The Function of HUD-Approved Real Estate Counseling

Financial obligation management does not exist in a vacuum. It is carefully connected to real estate stability. In Bloomington Credit Card Debt Consolidation, many people discover that their charge card financial obligation prevents them from certifying for a home loan or even keeping present rental payments. HUD-approved real estate counseling is a important resource provided by across the country firms. These services help people comprehend how their debt affects their real estate choices and offer techniques to safeguard their homes while paying down lenders. The combination of housing recommendations with debt management produces a more stable monetary structure for households throughout the 50 states.

In 2026, the connection in between credit rating and housing costs is tighter than ever. A lower debt-to-income ratio, attained through a structured management strategy, can lead to much better insurance coverage rates and lower mortgage interest. Therapy companies frequently partner with regional nonprofits and neighborhood groups to guarantee that these services reach diverse populations. Whether in a specific territory, the objective is to offer accessible financial literacy that translates into real-world stability.

Long-Term Strategy and Financial Literacy

Rolling over financial obligation in 2026 is as much about education as it is about interest rates. The most efficient programs consist of a deep focus on financial literacy. This involves finding out how to track expenses, construct an emergency situation fund, and understand the mechanics of credit report. Agencies that run across the country frequently offer co-branded partner programs with banks to assist consumers transition from financial obligation management back into conventional banking and credit products. This shift is a major turning point in the healing process.

The use of independent affiliates helps these firms extend their reach into smaller neighborhoods where specialized financial advice might be limited. By supplying these resources in your area, they guarantee that aid is readily available despite geography. For those in Bloomington Credit Card Debt Consolidation, this suggests access to the very same high-quality therapy found in major monetary centers. The method for 2026 is clear: stop the bleeding by decreasing interest rates, combine the process to ensure consistency, and use the resulting savings to construct an irreversible financial safeguard.

Handling financial obligation is a marathon. The 2026 environment needs a disciplined approach and a determination to seek expert assistance. By making use of the structures provided by nonprofit companies, individuals can browse the intricacies of contemporary credit. The procedure of moving from high-interest revolving financial obligation to a structured, negotiated plan is a proven course to financial health. With the ideal support and a concentrate on education, the debt that appears unmanageable today can be a thing of the past within simply a couple of years.

{kind=link}

Latest Posts

How Fair Credit Laws Are Progressing in 2026

Browsing the Complexity of Combination Loans in Your State

Professional Tips for Rolling Over Financial Obligation Next Year